Use of this website makes up acceptance of our Terms of Use, Personal Privacy Policy and also The Golden State Do Not Offer My Personal Information. NextAdvisor may get compensation for some links to product or services on this website. At NextAdvisor we're solid believers in transparency and also editorial independence. Editorial opinions are ours alone and have actually not been formerly reviewed, accepted, or backed by our partners. Editorial Visit this link web content from NextAdvisor is different from TIME editorial material and is produced by a different group of authors and editors. In December 1995, a government study ended that 50-- 60% of all Flexible Rate Home Loans in the United States have a mistake relating to the variable rates of interest charged to the home owner.

- Home mortgage repayments ballooned when the economic climate tanked, and also numerous debtors couldn't pay their new modified mortgage or refinance their escape of it.

- This allows debtors to get a much bigger finance (i.e., take on more financial debt) than would certainly or else be feasible.

- To get an understanding on what remains in shop for you with a variable-rate mortgage, you initially need to comprehend exactly how the product works.

- Adapting car loans are home mortgages that fulfill details standards that enable them to be sold to Fannie Mae and also Freddie Mac.

- Once your home deserves much less than the home mortgage, or the consumer sheds a work, they confiscate.

If you do not intend to reside in a residence much longer than the initial period of an ARM, you might save cash. If your plans change, you might need to re-finance to stay clear of the rate of interest modifications that can ruin your regular monthly budget plan. Many home owners pick an ARM to make use of the lower regular monthly home loan repayment throughout the introductory period, and also strategy to refinance or move prior to that duration finishes. If you intend on remaining in your house for a very long time, it's most likely best to take a look at a fixed-rate mortgage.

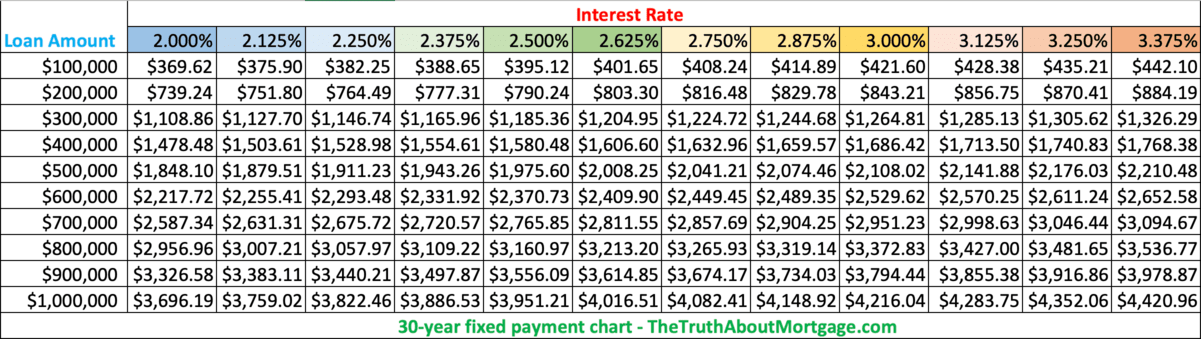

Fixed

Although there is the impending chance of a rates of interest walk after the initial duration, you can construct savings in the process to safeguard your financial resources versus this opportunity. Adjustable-rate mortgages can be the ideal move for borrowers intending to delight in the lowest feasible interest rate. Numerous lending institutions are willing to offer relatively low rates for the first period.

Other Kinds Of Arms

Charles Schwab & Co., Inc. does not solicit, use, recommend, negotiate or originate any kind of home loan products and is neither a licensed home mortgage broker neither a qualified home mortgage lending institution. Allow's consider just how 2 various kinds of home mortgages-- fixed-rate and adjustable-rate-- can offer different sorts of debtors, and exactly how their family member benefits can transform relying on dominating rate of interest. Mortgageloan.com is a website that provides info about home loans as well as car loans and does not supply financings or mortgages directly or indirectly through representatives or agents. We do not participate in straight advertising and marketing by phone or e-mail in the direction of consumers. Get in touch with our assistance if you are dubious of any type of fraudulent activities or if you have any kind of concerns.

When ARM rates readjust, the brand-new price is based upon a price index that shows current loaning problems. The brand-new rate will certainly be the index price plus a certain margin developed at the time you took out the finance. So if the index is at 3.5 percent when your rate readjusts and your margin is 2 percent, your new price will be 5.5 percent. Convertible ARM have the choice of converting their ARM into a fixed-rate home loan at a time marked in the home loan agreement. Home owners take pleasure in low introductory prices as well as the satisfaction that includes having a fixed-rate alternative. Once the fixed-rate section of the term mores than, the ARM readjusts up or down based upon current market rates, based on caps regulating just how much the price can go up in any specific modification.

An ARM might be. a superb choice if reduced payments in the near term are your main need, or if you don't prepare to stay in the building enough time for the prices to climb. As stated previously, the fixed-rate duration of an ARM differs, commonly from one year to seven years, which is why an ARM might not make sense for people who intend to keep their residence for even more than that. Nevertheless, if you recognize you are mosting likely to relocate within a brief period, or you do not prepare to hang on to the house for years ahead, after that an ARM is mosting likely to make a lot of sense.

Crossbreed ARMs are described by their preliminary fixed-rate and adjustable-rate periods, for example, 3/1, is for an ARM with a 3-year fixed interest-rate duration as well as succeeding 1-year interest-rate change periods. The date that a hybrid ARM shifts from a fixed-rate settlement routine to an adjusting payment routine is referred to as the reset day. After the reset date, a hybrid ARM floats at a margin over a specified index similar to any ordinary ARM. Most adjustable-rate mortgage options provide five, seven, or ten years.

Learn About Quicken Car Loans

Loaning criteria are stricter today than throughout the 2006 real estate bubble, Rugg noted. In the housing run-up greater than a decade ago, some lenders handed out so-called "liar's car loans," or home mortgages that called for little or no paperwork of earnings. Today, banks call for purchasers to validate their income to qualify for a lending. But economists state there are some distinctions in between today's pandemic housing boom and also 2006, such as banks' more stringent borrowing criteria. They consist of interest-only home loans, timeshares after death where debtors pay just http://donovancyyx861.tearosediner.net/acquire-to-market-home-mortgage the passion on their car loan for the very first 3 to one decade. She's additionally not a follower of payment-option ARMs, where debtors can pay much less interest than they owe in exchange for that interest getting added to the principal.